General questions about CSRD and ESRS

Click here to get answers on frequently asked questions about CSRD and ESRS in general.

ESRS is divided in 12 reporting standards: Cross cutting (General), Environmental, Social and Governance.

Select standard to see answers on Frequently asked questions:

ESRS 1 General requirements

ESRS 2 General disclosures

ESRS E1 Climate change

ESRS E2 Pollution

ESRS E3 Water and marine resources

ESRS E4 Biodiversity and ecosystems

ESRS E5 Resource use and circular economy

ESRS G1 Business conduct

General questions about CSRD and ESRS

What is ESRS?

How does ESRS relate to CSRD (Corporate Sustainability Reporting Directive)?

The ESRS are the standards developed as part of the CSRD, which is the directive that mandates sustainability reporting. ESRS provides the specific reporting requirements under this directive.

Which companies need to comply with ESRS?

ESRS applies primarily to large companies and all listed companies in the EU, including banks and insurance companies, irrespective of their size. The directive is aimed at ensuring that large enterprises contribute publicly on sustainability matters.

The schedule for companies to begin reporting under ESRS is as follows:

- Companies previously under the Non-Financial Reporting Directive (NFRD) — including large listed companies, large banks, large insurance undertakings, and large non-EU listed companies, all having over 500 employees — must start reporting from the financial year 2024. The first sustainability report will be due in 2025.

- Other large companies, including large non-EU listed companies, are to start from the financial year 2025, with their initial sustainability reports due in 2026.

- Listed SMEs, including non-EU listed SMEs, are set to begin from the financial year 2026, with the first reports to be published in 2027. However, these SMEs have the option to delay their reporting for up to two additional years. The latest they can start reporting is the financial year 2028, with their first sustainability reports appearing in 2029.

Moreover, non-EU companies that generate more than EUR 150 million annually in the EU and have either a branch with over EUR 40 million in turnover or a subsidiary classified as a large company, or a listed SME within the EU must start reporting on their group-level sustainability impacts starting from the financial year 2028. The initial sustainability report for these cases will be published in 2029, with specific standards set to be introduced for these circumstances.

What are the penalties for non-compliance with ESRS?

Penalties can vary by member state within the EU but generally include fines and potentially other sanctions such as mandatory audits or public disclosures of non-compliance.

What are the deadlines for compliance with ESRS?

The implementation dates vary, with the first reports expected for the fiscal year 2024, to be published in 2025. These timelines are staggered depending on the size and nature of the companies:

- Companies previously under the Non-Financial Reporting Directive (NFRD) — including large listed companies, large banks, large insurance undertakings, and large non-EU listed companies, all having over 500 employees — must start reporting from the financial year 2024. The first sustainability report will be due in 2025.

- Other large companies, including large non-EU listed companies, are to start from the financial year 2025, with their initial sustainability reports due in 2026.

- Listed SMEs, including non-EU listed SMEs, are set to begin from the financial year 2026, with the first reports to be published in 2027. However, these SMEs have the option to delay their reporting for up to two additional years. The latest they can start reporting is the financial year 2028, with their first sustainability reports appearing in 2029.

Moreover, non-EU companies that generate more than EUR 150 million annually in the EU and have either a branch with over EUR 40 million in turnover or a subsidiary classified as a large company or a listed SME within the EU must start reporting on their group-level sustainability impacts starting from the financial year 2028. The initial sustainability report for these cases will be published in 2029, with specific standards set to be introduced for these circumstances.

How will ESRS influence investor decisions?

By providing standardized and comparable sustainability information, ESRS will help investors make more informed decisions about where to allocate their resources, favouring companies with better sustainability practices.

Are there specific sectoral benchmarks in ESRS?

Yes, it will be. The ESRS includes specific benchmarks and metrics for different sectors to address sector-specific sustainability issues comprehensively. They have been delayed and are now announced to be implemented starting from the reporting year 2026.

What is the most difficult part of CSRD and ESRS reporting?

Many companies initially consider collecting quantitative data is the toughest part of ESRS reporting. However, they soon realize that the real challenge lies in the narrative disclosures. Over 70% of the ESRS Data point to disclose on are narrative, demanding detailed explanations that intertwine various aspects of the business such as value chain, business model(s), stakeholder interests, strategy, policies, targets, laws, specific disclosure requirements and more. Each narrative disclosure must consider these elements comprehensively, often requiring information scattered across multiple sections of the ESRS documentation.

To simplify this complex process, the Mentcon model is invaluable. The Mentcon model helps structure the sustainability report, providing prewritten text for nearly half of all narrative disclosures and offering templates of what to disclose with examples for the rest. This not only saves time and money but also ensures compliance with ESRS, making the reporting process significantly easier for companies.

What are the key components of ESRS?

The European Sustainability Reporting Standards (ESRS) comprise several key components designed to ensure comprehensive and uniform sustainability reporting across different sectors:

- General Disclosures: These include fundamental information about the organization, such as its business model, governance, and strategies related to sustainability, setting the context for more detailed disclosures. Included in the General disclosure is the foundation of ESRS, the Double Materiality. ESRS requires companies to report not only on how sustainability issues affect them (financial materiality) but also on how they impact society and the environment (impact materiality). The double materiality assessment defines what to be disclosed in:

- Environmental Disclosures: These focus on the organization’s impacts on the environment, covering aspects like climate change, resource use, pollution, and biodiversity.

- Social Disclosures: This component covers the organization’s impacts on social issues, including employee relations, human rights, community relations, and consumer protection.

- Governance Disclosures: These pertain to the governance structures and practices related to managing environmental, social, and governance (ESG) issues.

- (Sector-specific Disclosures: Tailored disclosures that address the unique environmental and social issues pertinent to specific sectors, providing detailed insights into industry-specific impacts and practices has been delayed and will be implemented starting from the reporting year 2026).

How to report and include ESRS, GRI and IFRS S2 in the same Sustainability statement?

When crafting a Sustainability Statement that aligns with multiple reporting standards like ESRS, GRI, and IFRS S2, companies can benefit significantly from integrated tools and methodologies like the Mentcon model. This simplifies the process and ensures comprehensive disclosure across different sustainability reporting standards:

- Using the Mentcon Model for ESRS Reporting: The Mentcon model is structured to assist companies in creating their Sustainability Statements according to the ESRS disclosure requirements. The model provides a solid foundation for reporting, ensuring that all required ESRS data points are thoroughly addressed.

- Integrating GRI and IFRS S2: Within the Mentcon model, companies have the complimentary option to include additional notes for GRI and IFRS S2. These notes are integrated into the Sustainability Statement by linking them to relevant sections via the respective GRI and IFRS S2 indexes. This means that for most of the data points required by these standards, corresponding information from the ESRS report can be directly referenced or automatically inserted.

- IFRS S2 Notes: The integration covers almost all the required disclosures, except for IFRS S2’s requirement under §29a (vi) related to Scope 3 financed emissions, which does not have a direct counterpart in ESRS. The Mentcon model app provides guidance on how and where to include this specific disclosure, ensuring that all necessary information is covered.

- GRI Notes: For GRI reporting, the integration through the Mentcon model is automatically cover about 90% of the information. For those GRI disclosure requirements that do not have a direct equivalent in ESRS, the Mentcon model app offers detailed instructions on how and where to report these items to ensure full compliance.

Overall, the Mentcon model facilitates a streamlined and effective way to incorporate ESRS, GRI, and IFRS S2 into a single Sustainability Statement, saving time, reducing errors, and enhancing the quality of reporting.

Should Disclosures pursuant to Article 8 of Regulation (EU) 2020/852 (Taxonomy Regulation) be included in the Sustainability statement?

Yes, it should be included in the Sustainability statement as shown in this table:

Structure of the ESRS sustainability statement

| Part of the management report | ESRS codification | Title | ||

|

ESRS 2 | General disclosures, including information provided under the Application Requirements of topical ESRS listed in ESRS 2 Appendix C. | ||

|

Not applicable | Disclosures pursuant to Article 8 of Regulation (EU) 2020/852 (Taxonomy Regulation) | ||

| ESRS E1 | Climate change | |||

| ESRS E2 | Pollution | |||

| ESRS E3 | Water and marine resources | |||

| ESRS E4 | Biodiversity and ecosystems | |||

| ESRS E5 | Resource use and circular economy | |||

|

ESRS S1 | Own workforce | ||

| ESRS S2 | Workers in the value chain | |||

| ESRS S3 | Affected communities | |||

| ESRS S4 | Consumers and end-users | |||

|

ESRS G1 | Business conduct |

How should companies prepare for ESRS reporting?

Companies should start by assessing their current reporting practices, identifying gaps in compliance with ESRS by conducting a Double materiality assessment. If using the Mentcon model for the Double materiality assessment, this will result in exactly which data points to report on, with descriptions of what to report – making it easy to identify gaps.

Companies might also need to implement new sustainability data management systems like Microsoft Sustainability Manager to capture necessary data if not already in place.

How to be able to report in the sustainability statement where all the 91 laws that derive from other EU legislation are disclosed?

In ESRS 2 Data point 56 “Disclosure of list of data points that derive from other EU legislation and information on their location in sustainability statement” shall be disclosed.

This is certainly very difficult and takes a lot of effort and time. The List of datapoints in cross-cutting and topical standards that derive from other EU legislation in ESRS 2 appendix 2 also have several errors in it which make it even more difficult. Mentcon have reported on all these errors, but these have not been updated yet.

This is a question we did not have a decent answer to. Therefore, we decided to develop a feature in Mentcon model App creating the list of data points that derive from other EU legislation and information on their location in sustainability statement—automatically in the sustainability statement!

The list is automatically inserted in ESRS 2 Data point 56 when following the Mentcon model.

The list created by the app includes:

- Disclosure Requirement and related paragraph in ESRS

- EU legislation:

- SFDR reference

- Pillar 3 reference

- Benchmark Regulation reference

- EU Climate Law reference

- Exactly where in the Sustainability statement the legislation is disclosed.

- If it is Material matter or not for the company

This auto-generated list in Mentcon model for ESRS fulfils this time-consuming disclosure requirement in an instant 😊

What tools are available to assist with ESRS compliance?

There are hundreds of software tools and platforms designed to help gather and manage sustainability data especially on GHG emissions. Sadly, almost all are just for collecting and calculating data.

Tools to collect and calculate climate data is available in the topic with questions on ESRS E1 Climate.

Specifically designed to aid in the structured preparation of the sustainability statements, the Mentcon model and its web application provide a robust framework for companies.

Mentcon model help describing the Business model, defining the value chain and the analysis of stakeholders to be able to do the Double materiality assessment. From the result of the materiality assessment of the company, Mentcon model creates the structure of the sustainability statement and which Data points to disclose on!

Mentcon model’s web application includes templates, tables, and pre-written text for more than over 1200 Data points in ESRS. This model not only helps organize and structure the sustainability report but also provides practical examples that demonstrate how companies addresses and reports on each of the required data points. By using such a specialized tool, companies can ensure that their reporting is comprehensive, aligned with best practices, and resonates with stakeholders.

Consultants and specialized firms also offer services to support compliance, which many of them using the Mentcon model.

ESRS 1 General Requirements

Here are some answers to Frequently Asked Questions about ESRS 1 General requirements.

What is ESRS 1 General requirements?

The objective of the standard ESRS 1 is to provide an understanding of the architecture of ESRS, the drafting conventions and fundamental concepts used, and the general requirements for preparing and presenting sustainability information in accordance with Directive 2013/34/EU (Accounting Directive), as amended by the Corporate Sustainability Reporting Directive (EU) 2022/2464 (CSRD).

What is the general requirement of ESRS 1 summarized?

The general requirements of the ESRS E1 encompass a comprehensive framework designed to guide entities in disclosing sustainability-related information. These requirements are structured to ensure disclosures align with the overarching directives of the European Union, specifically Directive 2013/34/EU and its amendments.

- Objective: ESRS aims to provide detailed disclosure requirements that allow stakeholders to understand an undertaking’s material impacts, risks, and opportunities concerning sustainability matters. These disclosures are essential for assessing the entity’s impact on environmental, social, and governance (ESG) aspects and the effects of these factors on its development and performance.

- Structure of ESRS: The standards are divided into:

- Cross-cutting standards that apply to all sectors,

- Topical standards focusing on specific ESG topics,

- Sector-specific standards that address unique industry concerns.

- Reporting Areas: Disclosures are categorized into four main areas:

- Governance: How governance structures manage ESG issues.

- Strategy: Interaction between the entity’s strategy and its sustainability impacts.

- Impact, Risk, and Opportunity Management: Processes for identifying and managing ESG matters.

- Metrics and Targets: Performance measures and progress indicators.

- Double Materiality: This principle dictates that reporting should reflect not only the financial impacts of sustainability matters on the entity but also the entity’s impact on the environment and society.

- Drafting Conventions: The standards specify terminology and the structure for disclosures, including a detailed explanation of terms like ‘impacts’, ‘risks’, and ‘opportunities’.

- Materiality: Entities must conduct a materiality assessment to determine which issues are significant enough to warrant disclosure based on their potential impact on stakeholders and the business itself.

- Qualitative Characteristics of Information: Information must be relevant, faithfully represented, comparable, verifiable, and understandable to meet the needs of diverse stakeholders.

- Value Chain Reporting: Information must extend to include not only the entity’s direct operations but also its upstream and downstream value chain impacts.

- Estimations and Proxies: When direct data collection is challenging, entities are permitted to use reasonable estimates or sector averages to provide the required information.

- Transitional Provisions: There are specific provisions for phased implementation, allowing entities time to adapt to the comprehensive reporting requirements.

What is the definition of double materiality?

Double materiality has two dimensions: impact materiality and financial materiality. A sustainability matter meets the criterion of double materiality if it is material from the impact perspective or the financial perspective or both.

What is Impact materiality in ESRS?

Definition Impact materiality in ESRS: A sustainability matter is material from an impact perspective when it pertains to the undertaking’s material actual or potential, positive, or negative impacts on people or the environment over the short-, medium- and long-term. A material sustainability matter from an impact perspective includes impacts connected with the undertaking’s own operations and upstream and downstream value chain, including through its products and services, as well as through its business relationships.

What is Financial materiality in ESRS?

Definition in Financial materiality in ESRS: A sustainability matter is material from a financial perspective if it generates risks or opportunities that affect (or could reasonably be expected to affect) the undertaking’s financial position, financial performance, cash flows, access to finance or cost of capital over the short, medium, or long term.

How to perform a double materiality assessment?

This is a summary of how the double materiality assessment is conducted according to the Mentcon model. Each step is described in more detail in referring questions and is very useful if not having access to the Mentcon model.

Step 1. Understanding Double Materiality

See previous questions:

- What is What is the definition of double materiality?

- What is Impact materiality in ESRS?

- What is Financial materiality in ESRS?

Step 2. Describe Business model(s) as it is.

Describing the Business model AS-IS represents a significant step towards establishing a shared understanding and comprehension of the organization, which will enable later steps in the process aimed at enhancing and advancing the company’s performance.

The business model of an undertaking is a foundational element that shapes how sustainability impacts, risks, and opportunities are identified, assessed, and managed. It provides context for understanding all sustainability-related activities.

The business model is a part of the Basics for conducting Materiality Assessment:

- Identifying potential Impacts and Risks and Opportunities: The business model helps in identifying which sustainability matters are potential material based on the business’s activities, resources, and relationships. This is crucial for focusing efforts on the most significant sustainability challenges and opportunities.

- Driving the Reporting Scope: The scope of sustainability reporting is significantly shaped by the business model, as it defines what the company does, how it creates value, takes actions and the resources it relies upon, which in turn determine the sustainability topics to be reported.

To define and analyse the business model, see question:

- How to define and analyze the Business model and use it throughout the Sustainability report in ESRS?

Step 3. Describe the Value chain

The description of the value chain should be focused on key value creation activities in the value chain. (The value chain is accompanied by the Business model and both shall be described and analyzed in to be able to conduct the Double materiality assessment and report on various disclosure requirements in ESRS).

For each part in the Value chain, Activities, Resources and Relationships shall be described and the position of the company in the value chain.

To Describe the value chain, see question:

- How to describe the value chain in ESRS?

Step 4. Conduct stakeholder analysis

The purpose of this step is to conduct a stakeholder analysis of stakeholders in the value chain and select stakeholders to include in the double materiality assessment in next steps (Called RIO-analysis in the Mentcon model app). It’s also a part of the due diligence process in Mentcon model.

Stakeholders are categorized into two main groups:

- Affected stakeholders: Individuals or groups impacted by the company’s activities, including those in the value chain.

- Users of sustainability statements: Investors, lenders, creditors, business partners, trade unions, NGOs, governments, analysts, and academics.

Engagement with stakeholders is crucial for identifying impacts and informing the materiality assessment.

To conduct stakeholder analysis, see question:

- How to conduct a stakeholder analysis?

Step 5. Choose Potential Material Matters

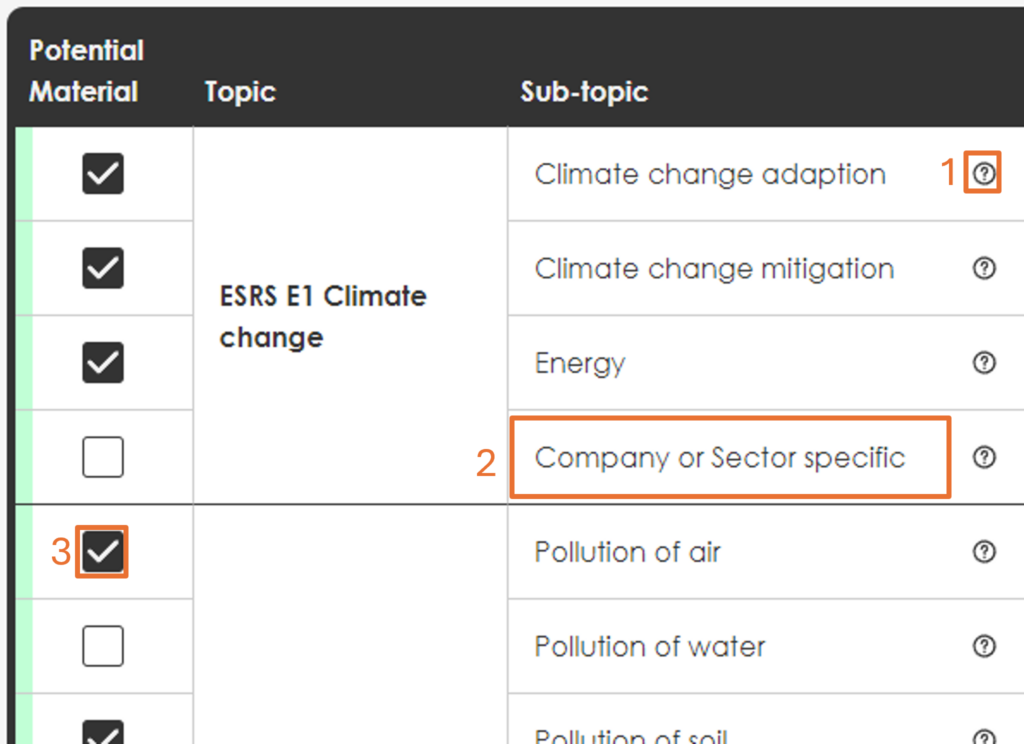

When performing the materiality assessment, Mentcon uses the list of sustainability matters covered suggested in ESRS AR 16. From this list, 24 potential material matters to make the materiality assessment from shall be chosen.

How to choose the potential material matters besides how the previous steps are included are described in Mentcon model and is and a brief summary of things to consider can be read here:

Start with the list of potentially significant sustainability issues that is built into the Mentcon model app, which utilises the ESRS suggested sustainability aspects:

- Consider the following background information to be able to select potentially sustainability matters:

- Understand the Context: Before a company begins identifying significant sustainability aspects, ensure to have a clear picture of the company’s operations, identify the value chains stakeholders (carried out in the previous step of the process Conduct stakeholder analysis of stakeholders in the value chain), and the geographical areas in which the company operates.

- Use existing information from the value chain:

- Customer satisfaction survey: (What do our customers think about various sustainability issues).

- Employee satisfaction survey: What can we find out from ours regarding harassment, equality, discrimination, etc.

- Supplier evaluations: What deviates in suppliers’ work and products as well as services from a sustainability perspective. It could be, for example, carbon footprint, emissions, child labour, adequate wages, etc.

- Other relevant industry and company-specific information.

- Consider the company’s strategy: Relate the sustainability risks to the company’s overall business strategy and objectives. A risk that can have a direct impact on the company’s core operations or brand should be given higher priority.

- Consider laws and regulations: Local, national, and international laws and regulations related to sustainability that affect [Company]. Some sustainability issues may be more significant due to legal requirements or expected regulatory changes.

- Consult experts in the value chain as needed. The Company/Group management determines the 24 significant sustainability aspects that a thorough double materiality analysis will be conducted on in the next step.

When choosing the Potential material matters in Mentcon model App perform these three steps in the image below:

- Click on the question mark to read definitions and generic examples to understand each potentially sustainability matter. (The app is available in 10 languages).

- If company- or sector-specific circumstances for significant issues emerge that are not included in the list, these significant issues are added to the list of Potential sustainability matters in the Mentcon model web application.

- Select 24 potential sustainability matters that will be used to conduct a double materiality assessment in the next step (called RIO-analysis in the Mentcon model app).

Step 6. Set Material Thresholds

According to ESRS undertakings shall apply the criteria for material impact and financial risk and opportunities, using appropriate quantitative and/or qualitative thresholds. Appropriate thresholds are necessary to determine which impacts, risks and opportunities are identified and addressed by the undertaking as material and to determine which sustainability matters are material for reporting purposes.

To set thresholds for material impacts and financial risks and opportunities, see question:

- How to set thresholds for material impacts and the financial risks and opportunities?

To see why the interpretations of material thresholds are so scattered between different consulting and accounting firms, read the following question, (it’s amusing, but important to understand to make it right):

- Our auditing firm are unable to provide clear guidance of setting material thresholds. Why are material thresholds so confusing?

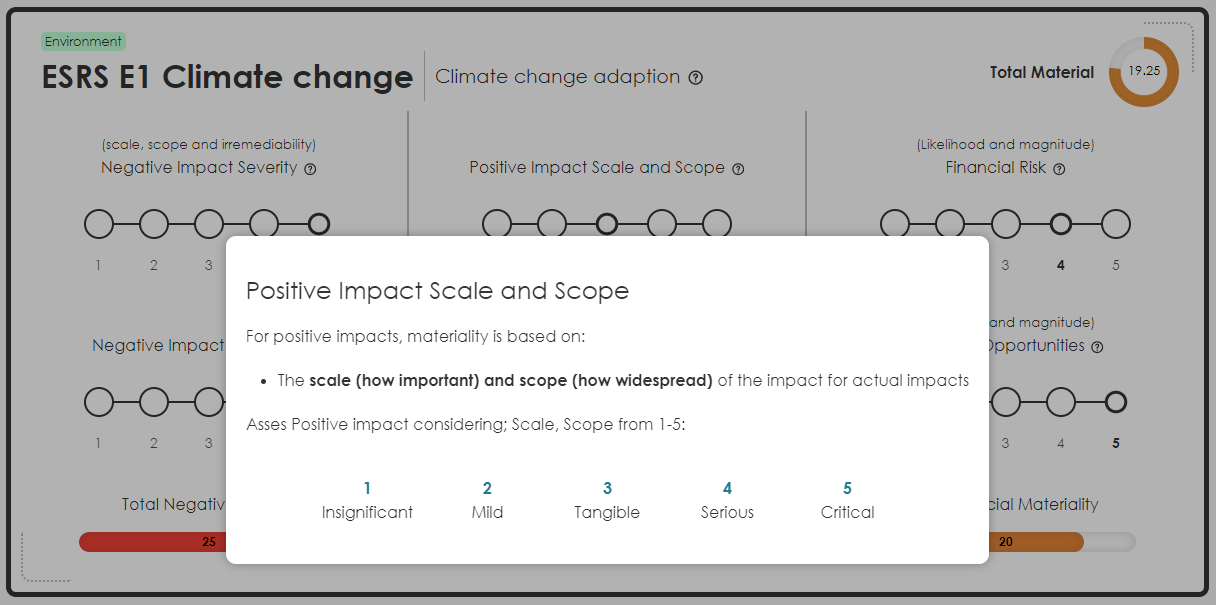

Step 7. Perform the Materiality Assessment

Based on the stakeholder analysis and the stakeholder that are invited to perform the Materiality assessment has received information how to conduct their questions to answer. The stakeholder can choose their preferred language to make the assessment easier to understand.

In the application each potential material matter is described using definitions from ESRS to make the assessment easier to understand and perform. Click the question mark to see the definitions.

The assessment is done through the double materiality perspective assessing impact and financial materiality.

Assessing Impact Materiality

Negative impact

The severity is based on the following factors:

- scale,

- scope, and

- reversibility. In the event of potential negative impacts for human rights, the severity of the impact is considered before its likelihood.

Positive impacts

For positive impacts, materiality is based on:

- the scale and extent of the impact for actual impacts, and

- the scale, extent, and likelihood of the consequence for potential impacts.

Assessing Finacial Materiality

- The risks and opportunities are assessed based on a combination of the likelihood of occurrence and the potential financial impact.

The assessment is made through a well-defined scale 1-5 for each part to assess. Click the question mark to see the definitions as illustrated in the image below:

Step 8. Weight And Decide On The Company’s Material Matters

This is a complex thing to do. There are many things to consider and fragments of this are described in different places in ESRS and key matters as thresholds are merely described at all.

Here will follow a few things to consider and after that the solution how to do.

Things to consider:

- Lack of Clear Criteria: ESRS lacks specific thresholds or detailed criteria for determining materiality. This can lead to inconsistencies in how different companies assess and report on material issues.

- Qualitative and/or Quantitative thresholds: Materiality assessments must incorporate qualitative judgments and/or quantitative data, but the exact thresholds or criteria for these assessments are not specified in ESRS.

- Stakeholder Engagement: The assessment must consider stakeholders views of materiality (Conducted in the materiality assessment).

- Qualitative vs Quantitative thresholds: What are quantitative thresholds? Is it subjective thought form certain stakeholders in the value chain and how should it be weighted in the overall picture? When performing a materiality assessment we got numbers, isn’t that quantitative data? We have some quantitative thresholds in our company, how can we know if they are low or high and how to weight it versus stakeholder views?

- Impact vs financial materiality: A sustainability matter meets the criterion of doublemateriality if it is material from the impact perspective or the financial perspective or both.

- Time horizons: This should be taken into account when assessing and determining on the material matters. In addition, sustainability issues are dynamic, and what is considered material can change over time as, customer demands, innovation, societal expectations and regulatory requirements evolve. ESRS does not provide a clear process for continuously updating materiality assessments to reflect these changes.

How to weight and decide on the company’s material matters:

In Mentcon model the process for conducting the double materiality assessment will be inserted into the sustainability statement automatically when following the process in Mentcon model App.

After doing the double materiality assessment in Mentcon model with stakeholders in the value chain, a result will be presented.

The result will be displayed in both graphical matrices and list:

- Negative impact

- Positive impact

- Total impact

- Financial risk

- Financial opportunities

- Total financial materiality

- Total materiality

- The result is also divided into the result from external respectively internal stakeholder in the value chain.

The stakeholder assessment in the Mentcon model App is to be weight against predefined quantitative thresholds in the earlier step of this process. (The Quantitative thresholds can be financial material thresholds and/or ecological impact thresholds based on frameworks as for example Science-Based Targets Initiative for Nature (SBTN) or other framework/initiatives).

The result of the double materiality assessment shall then be reviewed of internal experts as a part of the due diligence process.

Next step is to present the material matters for the entire senior management. Based on the material matters, the corporate management are responsible to take actions on material mattes, set its targets and report according to ESRS as defined in in later steps of Mentcon model.

When following the Mentcon model, the Board of the Company finally decides the material matters of the Company.

Step 9. Generate The Structure of The Sustainability Statement

When have decided on the material sustainability matters of the company in the Mentcon model App the structure of the sustainability statement and all Data points to report on is automatically generated!

All descriptions of the of the process to conduct the double materiality assessment, including description of the company’s business model, value chain, due diligence etc. will be automatically inserted into the corresponding Data points of the Sustainability statement.

Some Data points must be described company specific, and for these Data points templates and when appropriate tables are available. All Data points comes with examples from other companies of how to disclose, making it easy to understand what to disclose and finish the Sustainability statement.

How to know what to be reported in the Sustainability statement based on the double materiality assessment?

Determine Disclosure Content

- Identify required disclosures: Based on the double materiality assessment, identify which disclosures are required under the relevant ESRS standards. This is a real detective job and takes time. Plan for that. Take help of an auditor, if possible, already in this stage, to not get in problem in later stages because of reporting on incorrect Data points.

- Prepare entity-specific disclosures: If certain material aspects are not covered or insufficiently covered by existing ESRS, prepare entity-specific disclosures to ensure comprehensive reporting on these matters.

If using Mentcon model App: The disposition of the Sustainability statement and all datapoints to disclose on are generated automatically based on the double materiality assessment. Documentation of the materiality assessment process, criteria used, stakeholder engagement outcomes, and the rationale for determining the materiality of specific issues and more are automatically inserted under corresponding Data point!

What is Value chain in ESRS and how to use it?

The concept of the value chain in the European Sustainability Reporting Standards (ESRS) is extensive, capturing the entire spectrum of activities, resources, and relationships essential to the operation and impact of a business.

Definition of Value Chain in ESRS

The full range of activities, resources and relationships related to the undertaking’s business model and the external environment in which it operates.

A value chain encompasses the activities, resources and relationships the undertaking uses and relies on to create its products or services from conception to delivery, consumption and end-of- life. Relevant activities, resources and relationships include:

- those in the undertaking’s own operations, such as human resources;

- those along its supply, marketing and distribution channels, such as materials and service sourcing and product and service sale and delivery; and

iii. the financing, geographical, geopolitical and regulatory environments in which the undertaking operates.

Value chain includes actors upstream and downstream from the undertaking. Actors upstream from the undertaking (e.g., suppliers ) provide products or services that are used in the development of the undertaking’s products or services. Entities downstream from the undertaking (e.g., distributors, customers) receive products or services from the undertaking.

ESRS use the term “value chain” in the singular, although it is recognised that undertakings may have multiple value chains.

Brief Description of How to Use the Value Chain in ESRS

- Sustainability Assessment and Reporting

- Identify Material Impacts: Understand and assess how different segments of the value chain contribute to the sustainability impacts, risks, and opportunities. This is crucial for identifying which parts of the value chain might cause sustainability concerns or offer potential for positive sustainability contributions.

- Due Diligence Processes: Implement due diligence across the value chain to identify, prevent, mitigate, and account for negative sustainability impacts, and enhance positive impacts. This involves engaging with various value chain actors to ensure compliance with sustainability standards and practices.

- Disclosure and Transparency

- Sustainability Statement: Include detailed information about the value chain in the sustainability statement. This should cover how the undertaking manages its relationships with upstream suppliers and downstream customers to mitigate risks and leverage opportunities for sustainability.

- Extended Reporting: Report on the material impacts, risks, and opportunities associated with the value chain, extending the reporting beyond the immediate operations of the undertaking to include upstream suppliers and downstream customers.

- Engagement and Collaboration

- Stakeholder Engagement: Actively engage with stakeholders across the value chain to gather insights and feedback on sustainability practices, impacts, and improvement areas. This includes suppliers, customers, and other key actors who are part of the business ecosystem.

- Collaborative Initiatives: Participate in or initiate collaborative efforts with value chain partners to address common sustainability challenges such as reducing emissions, ensuring fair labor practices, and promoting circular economy practices.

- Management and Strategy Integration

- Strategic Decision-Making: Integrate value chain considerations into strategic planning and decision-making processes. This includes selecting suppliers based on sustainability criteria, designing products for lower environmental impact, and choosing distribution methods that minimize carbon footprints.

- Risk Management: Identify and manage risks that arise from the value chain, such as supply chain disruptions, compliance risks, or reputational risks related to suppliers’ practices.

- Enhancing Sustainability Practices

- Improvement and Innovation: Use insights from value chain analysis to drive sustainability innovations and improvements. This could involve developing new, more sustainable product lines, improving resource efficiency, or implementing more sustainable logistics solutions.

- Performance Metrics and Targets: Set specific, measurable targets for sustainability performance across the value chain and monitor progress through established metrics.

In conclusion, the value chain concept in ESRS is used to widen the scope of sustainability reporting and management, ensuring that an undertaking not only looks at its direct operations but also considers the broader network of activities and relationships that influence its sustainability footprint. By doing so, businesses can better manage their sustainability impacts and align more closely with global sustainability goals.

How to describe the value chain in ESRS?

A template is available in Mentcon model for ESRS web-app. The template is made based on the definition of Value chain according to CSRD and ESRS and encompassed to be able to answer on various disclosure requirements throughout ESRS. In the web-app the information about the value chain is automatically inserted in the equivalent Data points when generating the structure of the Sustainability statement.

Here’s a link to an article with an educational video of how to dexcribe the value chain, if your company not yet has access to our groundbreaking web-application:

How to describe the value chain in ESRS. Template and example included

Give an example of a description of a value chain and it’s main features for an ESRS Sustainability Statement?

Here is an example of a description of a value chain when using Mentcon model, included in this article:

How to describe the value chain in ESRS. Template and example included

Where comes the business model into the picture in ESRS and how shall it be used?

“Business model” is mentioned in ESRS 144 times and the Business model is a fundamental concept in the European Sustainability Reporting Standards (ESRS), particularly outlined in ESRS 1, which encompasses the general requirements for sustainability reporting.

Video of how to dislcose the business model in ESRS

Role of the Business Model in ESRS

- Integration into Sustainability Reporting:

- Foundational Element: The business model of an undertaking is considered a foundational element that shapes how sustainability impacts, risks, and opportunities are identified, assessed, and managed. It provides context for understanding all sustainability-related activities.

- Disclosure Requirements: ESRS requires that undertakings disclose how their business model interacts with their sustainability strategy and impacts. This includes explaining how the business model influences, and is influenced by, sustainability factors.

- Strategic Alignment:

- Alignment with Sustainability Goals: The business model must be aligned with sustainability goals, ensuring that sustainability considerations are embedded in core business strategies. This alignment helps in identifying areas where the business model can adapt to enhance sustainability outcomes.

- Informing Strategy and Business Model Adjustments: Sustainability considerations identified through the materiality assessment process (which includes examining the business model) should inform strategic adjustments to optimize sustainability performance.

Utilization of the Business Model in ESRS

- Materiality Assessment:

- Identifying Impacts and Risks: The business model helps in identifying which sustainability matters are material based on the business’s activities, resources, and relationships. This is crucial for focusing efforts on the most significant sustainability challenges and opportunities.

- Driving the Reporting Scope: The scope of sustainability reporting is significantly shaped by the business model, as it defines what the company does, how it creates value, and the resources it relies upon, which in turn determine the sustainability topics to be reported.

- Governance and Strategy Development:

- Guidance for Governance Structures: Understanding the business model aids in designing governance structures that are capable of managing sustainability issues effectively. This includes decisions about oversight, responsibilities, and the integration of sustainability into corporate governance.

- Strategy Formulation and Execution: Insights from the business model are used to craft sustainability strategies that are coherent with the business’s core operations and future objectives.

- Risk and Opportunity Management:

- Assessing Sustainability Risks: The business model analysis helps in pinpointing potential risks and vulnerabilities related to sustainability that the business might face, allowing for the development of mitigation strategies.

- Seizing Opportunities: Similarly, a clear understanding of the business model can reveal opportunities for sustainability innovations and enhancements that align with business operations and market positioning.

- Reporting and Disclosure:

- Comprehensive Disclosure: Companies are required to describe their business model within their sustainability statements, providing stakeholders with a clear understanding of how sustainability is integrated into the core business.

- Enhancing Transparency: Reporting on how the business model interacts with sustainability issues enhances transparency and helps stakeholders understand the business’s sustainability journey and commitments.

In summary, the business model in ESRS serves as a critical lens through which companies assess and report their sustainability impacts, risks, and opportunities. It guides strategic decisions, shapes governance practices, and informs comprehensive and transparent sustainability disclosures, ensuring that sustainability considerations are an integral part of the business’s core operations and strategic outlook.

How to define and analyze the Business model and use it throughout the Sustainability report in ESRS?

How to define the Business model(s) is not described in ESRS. As described in the earlier answer the Business model and its relation to different aspect is occurring over and over again in the disclosure requirements in ESRS.

To analyze it and use the business model throughout the Sustainability report is impossible to answer generally. Here is how it is solved when using Mentcon model:

In Mentcon model, how to describe and analyse the business model(s) are included. Explanations of how to disclose relevant information of the business model in the over hundred Data points is solved individually for each disclosure requirement. Some are inserted automatically based on the Company’s description of the business model in Mentcon model App. Others are disclosed with help of templates capturing the specific Data points disclosure requirements of how to disclose, with examples from other companies!

If not using Mentcon model, Osterwalders Business model canvas is suitable to describe the Business model(s) as a base for ESRS disclosure purposes.

Our auditing firm are unable to provide clear guidance of setting material thresholds. Why are material thresholds so confusing?

Our auditing firm are unable to provide clear guidance of setting material thresholds. Why is material thresholds so confusing?

First, it’s important to state. How to set thresholds for what’s material is not well defined in ESRS. Many companies and its consultants have been confused and makes severe mistakes. This is not strange. We will explain why the situation is confusing and provide information that helps to understand this, to facilitate reasoning with the consultants who will support you.

The Definition Confusion

- The definition of Material Threshold: Does not exist in ESRS, but is since long time defined in other contexts like GHG-protocol and means something completely different. In GHG-protocol: “A concept employed in the process of verification. It is often used to determine whether an error or omission is a material discrepancy or not. It should not be viewed as a de minimus for defining a complete inventory”.

- The Target Threshold: Target threshold is something different. It can be used to help a company to set a target when they already know what’s material. In ESRS target thresholds are mentioned in ESRS E2-E5 and refers to the Science-Based Targets Initiative for Nature (SBTN) and other framework/initiatives. Many consultancy- and even auditing firms unfortunately have mixt up target thresholds with material thresholds

- Confusing Text/Errors in ESRS: One example of error written in ESRS 1 § 42: Some existing standards and frameworks use the term “most significant impacts” when referring to the threshold used to identify the impacts that are described in ESRS as “material impacts.”

- We at Mentcon don’t know of any standard or framework using the term “most significant impacts”!?

- In this case, maybe ESRS refer to “Significance threshold” used in GHG-protocol and ecological frameworks. But the definition of Significance threshold is something entirely different: https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf.

Reasons for confusion

- Qualitative and/or Quantitative thresholds: Materiality assessments must incorporate qualitative judgments and/or quantitative data, but the exact thresholds or criteria for these assessments are not specified at all.

- Lack of Clear Criteria: ESRS lacks specific thresholds or detailed criteria for determining materiality. This can lead to inconsistencies in how different companies assess and report on material issues.

- Broad Scope of Considerations: ESRS requires considering a wide range of potential impacts and stakeholders, which can be overwhelming and open to interpretation. This broad scope makes it difficult to pinpoint which issues should be prioritized.

- Subjective Judgments: The reliance on qualitative judgments means that different companies might reach different conclusions about what is material, even when faced with similar circumstances. This subjectivity can reduce comparability and reliability across reports.

- Double Materiality Complexity: The dual focus on financial and impact materiality requires companies to evaluate issues from multiple perspectives, which can be complex and time-consuming. It also means that an issue might be material from an impact perspective but not from a financial one, or vice versa, adding another layer of complexity.

- Dynamic and Evolving Nature: Sustainability issues are dynamic, and what is considered material can change over time as, customer demands, innovation, societal expectations and regulatory requirements evolve. ESRS does not provide a clear process for continuously updating materiality assessments to reflect these changes.

How to set thresholds for material impacts and the financial risks and opportunities.

Setting thresholds for material impacts and financial risks and opportunities under the ESRS E1 General Requirements can be done in different ways depending on the type of potential material impacts, risk and opportunities.

Here is one more general example summarized, if not having access to the systematic approach of the Mentcon model to determine the thresholds of different sustainability matters for disclosure:

Step 1: Define the Scope of Assessment

- Identify all sustainability matters that might affect the entity or be affected by the entity’s operations, across its value chain. This includes environmental, social, and governance (ESG) factors.

- Determine the boundaries of the assessment, which could include direct operations, suppliers, customers, and broader community interactions.

Step 2: Prioritization Criteria

- Develop criteria to prioritize these matters based on their potential impact on the environment and society (impact materiality) and their potential to affect the entity’s financial condition (financial materiality).

- Consider the scale, scope, and severity of potential impacts, which involve the magnitude and range of the impact, as well as its possible permanence or reversibility.

Step 3: Stakeholder Engagement

- Engage with relevant stakeholders to understand their concerns and perspectives on what they consider significant sustainability matters.

- Incorporate stakeholder feedback to align the materiality thresholds with both stakeholder expectations and business priorities.

Step 4: Risk and Opportunity Analysis

- Analyze how identified sustainability matters could pose risks or present opportunities for the entity.

- Consider both short-term and long-term impacts, taking into account the entity’s strategic direction and operational context.

Step 5: Quantitative and Qualitative Thresholds

- Set quantitative thresholds where and if possible, such as percentage changes in revenue or costs, or specific environmental impact measures (e.g., tonnes of CO2 emissions).

- Define qualitative thresholds based on the nature of the impact or risk, such as changes in regulatory environments, shifts in consumer preferences, or impacts on employee welfare.

Step 6: Financial Materiality Considerations

- Assess the potential financial consequences of each sustainability matter, considering how they might influence investment decisions, financing costs, or operational expenses.

- Include considerations of dependencies on natural, human, and social capital, which could affect the entity’s ability to generate future economic benefits.

Step 7: Documentation and Review

- Document the rationale behind each threshold setting, ensuring that it is justifiable and understandable to external parties.

- Regularly review and update the thresholds as new information becomes available or as business and environmental conditions change.

Step 8: Integration into Reporting

- Integrate the results of the materiality assessment, including the set thresholds, into the entity’s sustainability reporting.

- Ensure clear disclosure of how thresholds were set and how they influence the reporting of material impacts, risks, and opportunities.

Formulärets överkant

This is still not easy. The materiality threshold in ESRS is often considered vague and confusing because it lacks the clear, concrete criteria The broad scope of considerations, reliance on subjective judgments, and the complexity introduced by the double materiality concept all contribute to this perception. Clearer guidelines and more specific criteria would help companies more consistently and accurately determine material sustainability issues.

Therefore, Mentcon have made it easy setting thresholds is an integrated feature of the Mentcon model, reducing subjectivity, addressing stakeholders, and setting clear thresholds for companies’ material matters. And yes of course, with the methodology used and the material thresholds inserted under the right Data points in the Sustainability statement automatically!

What is Due diligence according to ESRS 1 and how to conduct it?

Due diligence according to ESRS 1 is a systematic process that entities use to identify, prevent, mitigate, and account for how they address actual and potential negative impacts on the environment and people connected with their business. This process is integral to determining the material impacts, risks, and opportunities that should be disclosed in the sustainability statement.

Overview how due diligence is defined and should be conducted according to ESRS 1:

Definition of Due Diligence

- Due Diligence Process: ESRS defines due diligence as the ongoing practice of assessing and addressing the actual and potential negative impacts associated with an entity’s operations, products, services, and business relationships, including both upstream and downstream in the value chain.

- Framework Alignment: The process reflects the principles outlined in international frameworks such as the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises.

Summary of How to Conduct Due Diligence According to ESRS 1

Step 1: Embedding Due Diligence in Governance and Strategy

- Governance Integration: Ensure that sustainability matters are integrated into the governance structures. Information on sustainability matters should be regularly provided to and addressed by the administrative, management, and supervisory bodies.

- Strategy Inclusion: Incorporate considerations of sustainability risks and impacts into the entity’s strategy and business model planning. This includes how the entity plans to address these risks and impacts.

Step 2: Engaging with Stakeholders

- Identify Stakeholders: Determine who can affect or be affected by the entity’s operations — this includes employees, communities, suppliers, consumers, and more.

- Stakeholder Consultation: Engage with stakeholders to understand their concerns regarding the entity’s impacts on people and the environment. Use these insights to inform the due diligence process.

Step 3: Identifying and Assessing Impacts

- Impact Assessment: Identify both actual and potential negative impacts connected with the entity’s own operations and its value chain. Prioritize impacts based on their severity and likelihood.

- Risk and Opportunity Assessment: Assess how these impacts translate into risks and opportunities for the entity, considering both the short and long term.

Step 4: Taking Action

- Mitigate Negative Impacts: Develop and implement actions to prevent or mitigate identified negative impacts. This could include changing operational practices, enhancing worker safety protocols, or modifying supply chain management.

- Remediation Plans: Establish processes to remediate any harm caused by the entity’s operations or business relationships.

Step 5: Tracking Effectiveness

- Monitor and Review: Continuously monitor the effectiveness of the measures taken to address sustainability impacts and adjust strategies as necessary.

- Reporting and Transparency: Regularly report on the progress and effectiveness of due diligence actions in the sustainability statement.

Step 6: Public Reporting and Accountability

- Disclosure: Disclose due diligence processes, findings, and actions in the sustainability statement. This includes detailing how negative impacts are addressed and how stakeholder engagement has informed the due diligence process.

Incorporating Due Diligence into the Sustainability Statement

- Comprehensive Reporting: Ensure that the sustainability statement reflects the comprehensive due diligence process. This should include a discussion of governance practices, stakeholder engagement outcomes, impact assessments, actions taken, and the effectiveness of these actions.

Due diligence is incorporated into Mentcon model and how it has been conducted shall be documented in many Data points in the sustainability statement. When following the Mentcon model process this will be described with pre-written text inserted automatically in the corresponding Data points.

I don’t understand Incorporation by reference described in ESRS 1 section 9.1. Explain with examples.

In BP-2 – Disclosures in relation to specific circumstances Data point 16, a list of incorporation by references shall be disclosed.

Since information such as the business model and value chain might already be disclosed elsewhere (for example, in the management report), using references can help avoid redundant reporting.

Below is an example list of how to disclose such a list with typical information to incorporate by reference:

List of ESRS Disclosures Incorporated by Reference

ESRS 2, General Disclosure SBM-1:

Referenced Source: Management report.

Specific Datapoints: Description of Business model and Value chain. ESRS 2 SBM-1 Datapoint 42 and 42c.

ESRS E1, Climate Change ESRS 2 SBM-3 E1:

Referenced Source: Universal Registration Document, Article on Environmental Strategy.

Specific Datapoints: Details on resilience planning for climate-related risks: ESRS E1 SBM-3 Datapoint 19b-c.

ESRS S1:

Referenced Source: Financial Statements.

Specific Datapoints: Details on employment figures, within the financial overview: ESRS 2 SBM-1 Data point 40 a iii, ESRS S1 S1-6 50a and 50c.

ESRS Own Workforce S1-4:

Referenced Source: Corporate Governance Statement.

Specific Datapoints: Information on initiatives for employee health and safety, mental health support programs, and workplace ergonomics: ESRS S1 Data point 37, 38 a-d.

ESRS Business Conduct G1:

Referenced Source: Remuneration Report required by Directive 2007/36/EC.

Specific Datapoints: Disclosures on executive remuneration policies linked to ethical business practices and anti-corruption measures: ESRS S1 Data point 97b, ESRS 2 GOV-3 Data point 29 and 29c.

ESRS E4 Biodiversity and Ecosystems:

Referenced Source: EMAS Report.

Specific Datapoints: Information on land-use using guidance provided by the Eco-Management and Audit Scheme (EMAS): ESRS E4 Data point AR 34 a-d.

ESRS 2 General Disclosures

Here are some answers to Frequently Asked Questions about ESRS 2.

What is the objective of ESRS 2 General Disclosures?

The objective of ESRS 2 General Disclosures, is to provide a framework for all undertakings to disclose sustainability information that is sector-agnostic and applicable across various sustainability topics. This standard is designed to ensure that organizations report on sustainability issues comprehensively, covering the cross-cutting standards and reporting areas defined in ESRS 1 General Requirements.

ESRS 2 General Disclosures sets out the disclosure requirements that every undertaking must follow when preparing their sustainability statements, regardless of their specific sector or the unique sustainability challenges they face. This includes applying the General disclosure requirements and their associated datapoints from topical ESRS as specified in Appendix C of the standard:

|

ESRS 2 Disclosure Requirement |

Related ESRS paragraph |

|

GOV–1 The role of the administrative, management and supervisory bodies |

ESRS G1 Business conduct (paragraph 5) |

|

GOV–3 Integration of sustainability-related performance in incentive schemes |

ESRS E1 Climate change (paragraph 13) |

|

SBM–2 Interests and views of stakeholders |

ESRS S1 Own workforce (paragraph 12) ESRS S2 Workers in the value chain (paragraph 9) ESRS S3 Affected communities (paragraph 7) ESRS S4 Consumers and end-users (paragraph 8) |

|

SBM–3 Material impacts, risks and opportunities and their interaction with strategy and business model |

ESRS E1 Climate Change (paragraphs 18 to 19) ESRS E4 Biodiversity and ecosystems (paragraph 16) ESRS S1 Own workforce (paragraph 13 to 16) ESRS S2 Workers in the value chain (paragraph 10 to 13) ESRS S3 Affected communities (paragraph 8 to 11) ESRS S4 Consumers and end-users (paragraph 9 to 12) |

|

IRO-1 Description of the processes to identify and assess material impacts, risks and opportunities |

ESRS E1 Climate change (paragraph 20 to 21) ESRS E2 Pollution (paragraph 11) ESRS E3 Water and marine resources (paragraph 8) ESRS E4 Biodiversity and ecosystems (paragraph 17 to 19) ESRS E5 Resource use and circular economy (paragraph 11) ESRS G1 Business conduct (paragraph 6) |

These requirements are mandatory for descriptions of the processes to identify and assess material impacts, risks, and opportunities (IRO-1) and apply to other requirements only if the related sustainability topic is deemed material according to the undertaking’s materiality assessment, rooted in the principle of double materiality as outlined in ESRS 1.

Are there any templates and tools or frameworks provided for ESRS 2 General Disclosures?

- EFRAG IG 1: Materiality assessment implementation guidance

- EFRAG IG 2: Value chain implementation guidance

However, these have been criticised to give more questions than answers but no new versions of them will be published. For now, companies are encouraged to follow the guidelines outlined in the ESRS documents, which provide a structure to what information should be included.

Businesses may also turn to industry groups, consultants, or sustainability organizations that may offer templates or software tools designed to align with ESRS and other sustainability reporting frameworks to assist in compliance.

A framework that has interpreted all disclosure requirements to become compliant with ESRS 2 is the Mentcon model. It includes step-by-step process to disclose on ESRS 2 with a supporting web application including:

- Business model

- Value chain

- Stakeholder analysis

- Resulting in stakeholders in the value chain to include in the double materiality assessment

- Double materiality assessment

- Due diligence

- Risk management and internal control

- Interest and views of stakeholders

- Description of the process to identify and Assess Material Impacts, Risks, and Opportunities

- Generation of the Sustainability statement and the data points to disclose on based on the materiality assessment

- Pre-written disclosures of how the company has conducted steps in the process for Data points requiring such disclosures in ESRS (when following the Mentcon model process)

- Templates, tables with examples to how and what to disclose on all Data points the company must disclose on, including the voluntary Data points

What are the disclosure requirements under ESRS 2 General disclosures?

Here is a table of content of Disclosure requirements under ESRS 2 General disclosures.

All these disclosures are explained in a straightforward manner, each addressed separately in the following questions.

Basis for preparation

BP-1 – General basis for preparation of the sustainability statement

BP-2 – Disclosures in relation to specific circumstances

Governance

GOV-1 – The role of the administrative, management and supervisory bodies

GOV-2 – Information provided to and sustainability matters addressed by the undertaking’s administrative, management and supervisory bodies

GOV-3 – Integration of sustainability-related performance in incentive schemes

GOV-4 – Statement on due diligence

GOV-5 – Risk management and internal controls over sustainability reporting

Strategy

SBM–1 Strategy, business model and value chain

SBM-2 – Interests and views of stakeholders

SBM-3 – Material impacts, risks and opportunities and their interaction with strategy and business model

Impact, risk and opportunity management

IRO-1 – Description of the process to identify and assess material impacts, risks and opportunities

IRO-2 – Disclosure requirements in ESRS covered by the undertaking’s sustainability stateme

Minimum disclosure requirement on policies and actions

Minimum Disclosure Requirement – Policies MDR-P – Policies adopted to manage material sustainability matters

Minimum Disclosure Requirement – Actions MDR-A – Actions and resources in relation to material sustainability matters

Metrics and targets

Minimum Disclosure Requirement – Metrics MDR-M – Metrics in relation to material sustainability matters

Minimum Disclosure Requirement – Targets MDR-T – Tracking effectiveness of policies and actions through targets

Below are all the Disclosure requirements of ESRS 2.

If you want an more details and a video introduction, read more here in this article: ESRS 2 General Disclosures Requirements Summarized | Mentcon

Basis for Preparation

The “Basis of Preparation” in ESRS 2 pertains to the fundamental requirements and guidelines for how companies should prepare their sustainability statements, ensuring clarity, consistency, and comprehensibility for all stakeholders. Key aspects in Basis for preparation in ESRS includes BP-1 and BP-2.

BP-1 – General basis for preparation of the sustainability statement

Preparation Scope

Companies must state whether the sustainability statement is prepared on a consolidated basis or for an individual entity.

Scope of Consolidation

For consolidated statements, it must be confirmed whether this scope matches that of the financial statements or explain any deviations.

Value Chain Coverage

The extent of the sustainability statement’s coverage over the company’s upstream and downstream value chain should be detailed.

Omission of Sensitive Information

Companies may omit sensitive information related to intellectual property or innovations, and must declare if any exemption has been used for non-disclosure of pending developments or negotiations.

BP-2 – Disclosures in relation to specific circumstances

This involves disclosing any unique or specific conditions affecting the preparation of the sustainability statement, aiming to elucidate the impact of these circumstances on the presented sustainability information.

Time Horizons

Companies must describe their own definitions of medium or long-term time horizons, especially if they deviate from the standard definitions provided by ESRS, and explain the reasons for these definitions.

Value Chain Estimation

When sustainability metrics involve estimated data from the value chain using proxies like sector averages, companies should explain the basis of these estimates, the accuracy levels, and future steps to improve this accuracy.

Sources of Estimation and Outcome Uncertainty

Companies need to identify which parts of their disclosed information involve significant estimation uncertainty and explain the sources and assumptions behind these estimates.

Changes in Preparation or Presentation of Sustainability Information

Companies are required to explain any changes made to the preparation and presentation methods of sustainability information compared to prior periods. This includes providing reasons for these changes, presenting revised comparative figures where possible, or explaining why such adjustments were impracticable.

Reporting Errors in Prior Periods

If material errors from previous periods are identified, companies must disclose the nature of these errors, corrections made for each prior period as feasible, and explain any impracticability in making corrections.

Disclosures Stemming from Other Legislation or Generally Accepted Sustainability Reporting Pronouncements:

When a sustainability statement includes information required by other legislation or generally accepted sustainability standards and frameworks, companies must disclose this fact. If only parts of other standards are applied, the specific paragraphs applied must be referenced.

Incorporation by Reference

Companies can incorporate certain information by reference, indicating which parts of the ESRS or specific datapoints are included in this manner. This approach is intended to avoid duplication and enhance clarity by referring to information provided elsewhere.

Use of Phase-In Provisions in Accordance with Appendix C of ESRS 1:

Smaller entities or groups, specifically those with fewer than 750 employees, can opt to omit information required by other specific ESRS standards but must still disclose if the sustainability topics covered by these omissions have been assessed as material. For each material topic, companies must disclose a variety of details including the relevant issues assessed, the targets set, policies, actions taken, and relevant metrics.

Governance

In ESRS 2, governance is detailed to ensure organizations disclose the structures, processes, and strategies employed to oversee and manage sustainability-related matters effectively. These are disclosed in GOV-1 – GOV 5.

GOV-1 - The Role of the Administrative, Management, and Supervisory Bodies

Disclosure Requirement GOV-1 – The Role of the Administrative, Management, and Supervisory Bodies outlines the necessity for organizations to provide detailed information on the structure, roles, responsibilities, and capabilities of their governing bodies in relation to sustainability oversight. This disclosure requirement aims to give stakeholders a clear understanding of how sustainability matters are governed within the organization.

Summary of key requirements of ESRS GOV-1:

Composition and Diversity

Organizations must disclose the makeup of their administrative, management, and supervisory bodies, including the number of executive and non-executive members, representation of employees, and diversity aspects such as gender and independence. This includes detailing the percentage of independent members, which varies depending on the structure of the board (unitary or dual).

Roles and Responsibilities

The disclosure should clearly outline the specific roles and responsibilities of the administrative, management, and supervisory bodies in managing sustainability-related impacts, risks, and opportunities. This includes information on how these responsibilities are incorporated into the organization’s governance frameworks, such as terms of reference and board mandates.

It should also describe the processes and controls these bodies use to oversee these sustainability matters, including how management roles are defined, the delegation of responsibilities to specific positions or committees, and the reporting lines to higher governance bodies.

Expertise and Skills

The requirement emphasizes the need for these bodies to possess or have access to the necessary expertise and skills related to sustainability. Organizations must describe the sustainability-related competencies of their governing bodies and how these are applied or developed, including the use of training programs or external experts.

Monitoring and Target Setting

Organizations must explain how their governance bodies participate in setting and monitoring targets related to significant sustainability impacts, risks, and opportunities. This includes an overview of the mechanisms and processes in place to track progress and make adjustments as necessary.

GOV-2 - Information Provided to and Addressed by the Governance Bodies

Disclosure Requirement GOV-2 – Information Provided to and Addressed by the Governance Bodies focuses on the communication and decision-making processes related to sustainability within an organization’s governing bodies. This requirement aims to ensure transparency in how these bodies are kept informed about sustainability issues and how they address them. It also assesses the adequacy and effectiveness of this information flow in enabling these bodies to perform their oversight responsibilities effectively.

Summary of key requirements of ESRS GOV-2:

Information Flow

Organizations must disclose the mechanisms through which their administrative, management, and supervisory bodies are informed about sustainability-related matters. This includes detailing who provides the information, how often it is provided, and the nature of the information related to material impacts, risks, and opportunities.

The disclosure should also cover the processes of implementing due diligence and the effectiveness of policies, actions, metrics, and targets set for addressing sustainability matters.

Decision-Making Processes

The requirement highlights the need to disclose how the governance bodies use the information received to make decisions regarding the organization’s strategy, major transactions, and risk management. This includes how these bodies assess and weigh the trade-offs associated with various sustainability impacts, risks, and opportunities.

Addressing Material Impacts, Risks, and Opportunities

Organizations must list the specific material impacts, risks, and opportunities that were addressed by the governance bodies during the reporting period. This should include a discussion on how these matters were handled, providing insight into the effectiveness of the governance structure in managing sustainability issues.

Importance of ESRS GOV-2

This disclosure helps stakeholders understand the role and effectiveness of an organization’s governance bodies in managing sustainability. It ensures that the governance structures are not only informed but are actively engaging with and addressing sustainability challenges. By showcasing how information is used to guide strategic decisions and risk management, GOV-2 reinforces the accountability and responsiveness of governance bodies to sustainability issues, enhancing stakeholder confidence in the organization’s sustainability governance.

GOV-3 - Integration of Sustainability-Related Performance in Incentive Schemes

Disclosure Requirement GOV-3 – Integration of Sustainability-Related Performance in Incentive Schemes, focuses on the ways in which sustainability performance influences compensation within an organization. This requirement compels an undertaking to disclose if and how its incentive schemes for the administrative, management, and supervisory bodies incorporate sustainability-related criteria.

Key Characteristics of Incentive Schemes

The company must describe the main features of the incentive schemes that are applicable to the governance bodies. This includes the general structure and basis of the incentives, emphasizing the integration of sustainability goals.

Assessment Against Sustainability Targets/Impacts

It should be disclosed whether the performance evaluations for incentive schemes consider specific sustainability-related targets or impacts. If so, the details of these targets or impacts must be specified, explaining how they are measured and evaluated.

Use of Sustainability Metrics in Remuneration Policies

The disclosure should state whether sustainability-related performance metrics are used as benchmarks in the remuneration policies of the company. This includes how these metrics are incorporated into the overall evaluation process for determining compensation.

Proportion of Variable Remuneration Linked to Sustainability

The undertaking needs to specify the proportion of variable compensation (bonuses, stock options, etc.) that is tied directly to achieving sustainability-related targets or managing sustainability impacts.

Approval and Update of Incentive Terms

Information must be provided about the organizational level at which the terms of these incentive schemes are approved and the frequency with which they are reviewed or updated. This helps in understanding the governance structures in place for overseeing the alignment of incentives with sustainability performance.

GOV-4 - Statement on Due Diligence

Disclosure Requirement GOV-4, “Statement on Due Diligence,” concerns the transparency of an organization’s due diligence processes related to sustainability matters. This requirement emphasizes how these processes are integrated and depicted within the organization’s sustainability statement. Overviev of what should be disclosed under GOV-4:

Mapping the Due Diligence Process

The organization must provide a detailed mapping that demonstrates how and where each aspect and step of its due diligence process is reported within the sustainability statement. This mapping should clearly show the linkage between the reported information and the specific due diligence practices implemented by the organization.

Objective of the Disclosure

The main goal of this disclosure requirement is to enhance the understanding of the organization’s due diligence processes concerning sustainability matters. It aims to ensure that stakeholders can clearly see how the organization identifies, assesses, and manages the sustainability-related impacts, risks, and opportunities.

Detailed Explanation of Due Diligence Practices

The undertaking should detail the main aspects and steps involved in its due diligence process as defined under ESRS 1, Chapter 4 (“Due Diligence”). This should include how these practices are applied across various domains of the organization and how they relate to both cross-cutting and specific topical disclosure requirements under the ESRS framework.

Non-Prescriptive Nature of the Requirement

It is important to note that GOV-4 does not impose specific behavioral actions regarding due diligence, nor does it modify the existing roles of the administrative, management, and supervisory bodies as prescribed by other legislations or regulations. Instead, it focuses on reporting and transparency of existing processes.

Illustration of Actual Practices