How to know what to disclose specifically for your company in ESRS E1, what are the disclosure requirement and an educational video is included in this article.

What is ESRS E1 Climate Change and its main objective?

The objective of ESRS E1 Climate Change is to provide comprehensive disclosure requirements that enable stakeholders to understand the full spectrum of an undertaking’s influence on, and response to, climate change, including:

Impact Analysis. Detailing how the undertaking contributes to climate change through both positive and negative impacts, addressing both actual and potential effects.

Mitigation Efforts. Outlining the actions taken by the undertaking to mitigate its contributions to global warming, ensuring these efforts align with international agreements like the Paris Agreement, aiming to limit global warming to 1.5°C.

Adaptation Strategies. Describing the undertaking’s strategies and capacities for adapting its business model to support a sustainable economy and contribute effectively to climate change mitigation.

Comprehensive Action Review. Reporting on additional actions taken to prevent, mitigate, or remediate negative climate impacts, along with how the undertaking manages related risks and opportunities.

Risk and Opportunity Management. Providing insights into the material risks and opportunities related to climate change that affect the undertaking, detailing how these are managed.

Financial risk and opportunities. Discussing the short-, medium-, and long-term financial implications of climate-related risks and opportunities on the undertaking.

How to know what to disclose for your company in ESRS E1

Note! All these 12 sections of disclosures below might not have to be disclosed depending on what’s material for the company concerning climate change. (The logic of what to disclose is included in the Mentcon model for the ESRS web-app to make companies aware of what to disclose, based on the draft of ID 177 – Links between AR16 and Disclosure requirements, and will be updated in the Mentcon model if any changes are made in the final version).

Read more about Mentcon model for ESRS: Mentcon model for ESRS

Examples:

If climate change mitigation is not material to the company, for example, E1-6 does not have to be disclosed!

Non-relevant disclosures don’t have to be disclosed. For example, E1-8 internal carbon pricing when not used by a company.

E1-9 does not have to be disclosed if none of the material sustainability matters of climate change are material from a financial perspective, even though it is material from an impact perspective.

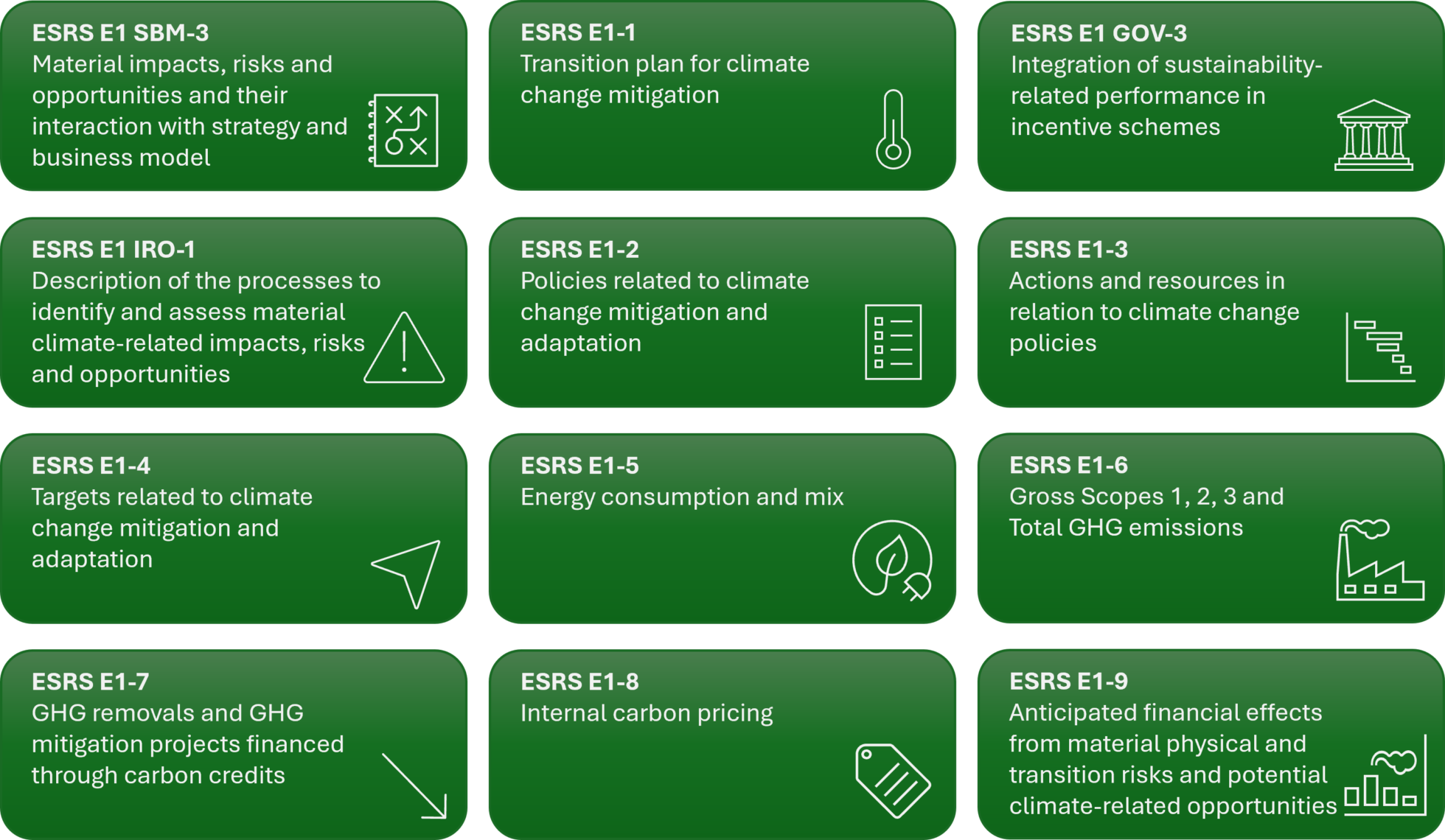

Summary of the disclosure requirements of ESRS E1 Climate Change

ESRS E1 GOV-3 Integration of Sustainability-Related Performance in Incentive Schemes

This disclosure requirement emphasizes the alignment of sustainability goals with the company’s performance-based incentive schemes. It mandates that companies disclose how sustainability-related performance metrics, particularly those linked to climate change mitigation and adaptation, are incorporated into employee or management incentive structures.

In practice, companies must explain, if having sustainability-related performance in Incentive schemes:

- Which sustainability metrics are integrated into incentives (e.g., GHG emissions reduction, energy efficiency improvements).

- Who is impacted by these incentives, such as key management personnel or employees across the organization.

- The degree of financial impact, outlining how achieving sustainability goals ties directly to compensation or bonuses.

E1-1 Transition Plan for Climate Change Mitigation

Disclosure Requirement E1-1 focuses on a company’s transition plan to mitigate climate change, ensuring alignment with global warming limits of 1.5°C as per the Paris Agreement. The transition plan must:

- Outline how GHG reduction targets (as per E1-4) align with the 1.5°C goal.

- Identify key decarbonization levers and actions, such as changes in product offerings, technological upgrades, and shifts in operations or value chains.

- Highlight investments and funding committed to achieving the plan, such as CapEx aligned with EU Taxonomy regulation.

- Assess potential locked-in GHG emissions from key assets and explain how they might affect future transition risks.

- Explain how the transition plan is integrated into the broader business strategy and whether it has been approved by senior management.

This disclosure requirement helps stakeholders understand how a company is planning to reduce its carbon footprint and transition to a low-carbon economy.

ESRS E1 SBM-3: Material Impacts, Risks, and Opportunities and Their Interaction with Strategy and Business Model

Under SBM-3, companies must describe how climate-related risks, impacts, and opportunities interact with their business model and strategy.

- Identify physical and transition risks related to climate change, distinguishing between risks from physical impacts (e.g., extreme weather) and those from transitioning to a low-carbon economy (e.g., regulatory changes).

- Evaluate the resilience of their strategy and business model to these risks, including the scope of the analysis and the use of scenario analysis to assess different climate futures.

- Outline how these risks and opportunities influence key business decisions, ensuring the organization is strategically prepared for future climate-related challenges and opportunities.

This disclosure ensures transparency about how climate-related risks are embedded in a company’s strategic planning.

ESRS E1 IRO-1 Description of the Processes to Identify and Assess Material Climate-Related Impacts, Risks, and Opportunities

The IRO-1 requirement asks companies to describe the processes they use to identify and assess climate-related impacts, risks, and opportunities. Key areas of disclosure include:

- GHG emissions: How the company assesses its impacts on climate change through GHG emissions.

- Physical risks: Identifying climate hazards that could affect operations, including extreme weather or chronic shifts in climate patterns.

- Transition risks: Understanding how policy, technological, and market shifts may create risks or opportunities for the company.

- Scenario analysis: Explaining how different climate scenarios have informed the identification and assessment of these risks and opportunities over the short, medium, and long term.

This disclosure provides insight into the robustness of the company’s risk management processes and its ability to anticipate and adapt to climate-related changes.

E1-2 Policies Related to Climate Change Mitigation and Adaptation

Disclosure Requirement E1-2 focuses on the policies that the company has adopted to address climate change mitigation and adaptation. This requirement aims to provide a clear understanding of the company’s overall governance and strategic direction concerning climate-related impacts, risks, and opportunities.

Key elements of E1-2:

- Climate change mitigation: The company must describe policies designed to reduce GHG emissions, including those that promote energy efficiency, the transition to renewable energy, and decarbonization efforts. These policies should aim at reducing the company’s carbon footprint and align with global climate goals, such as limiting global warming to 1.5°C.

- Climate change adaptation: Policies that address how the company is preparing for the impacts of climate change, such as changes in weather patterns, rising sea levels, or increased frequency of extreme events. This may include infrastructure upgrades, supply chain resilience, and risk management strategies to cope with climate-related physical risks.

- Energy efficiency and renewable energy: The company must detail its policies that promote energy efficiency and the deployment of renewable energy sources. This includes policies on reducing energy consumption and increasing the share of energy derived from renewable sources, such as solar, wind, or bioenergy.

Additionally, the disclosure should reflect how these policies are integrated into the company’s overall sustainability strategy.

E1-3 Actions and Resources in Relation to Climate Change Policies

This requirement builds on E1-2 by focusing on the actions taken and the resources allocated to implement the climate change policies disclosed. The goal is to give stakeholders an understanding of the concrete steps the company is taking to achieve its climate-related objectives.

- Key actions: The company should list the key actions taken during the reporting period to mitigate climate change, such as investment in low-carbon technologies, energy efficiency programs, and partnerships for renewable energy projects. Future planned actions should also be disclosed, emphasizing long-term commitments.

- Decarbonization levers: The company must describe specific decarbonization levers used to reduce GHG emissions. These may include nature-based solutions (e.g., afforestation projects), electrification of operations, energy transitions, or product and process changes aimed at lowering emissions.

- Resource allocation: Companies must disclose the financial resources (CapEx and OpEx) allocated to these actions. This includes significant monetary investments in carbon reduction projects, green infrastructure, and research & development into sustainable technologies. The disclosure must link these expenditures to relevant financial statements or notes.

The disclosure also requires the company to highlight any expected or achieved outcomes of these actions, such as reductions in GHG emissions, improved energy efficiency, or advancements in renewable energy adoption.

E1-4 Targets Related to Climate Change Mitigation and Adaptation

Under E1-4, companies must disclose the climate-related targets they have set to support their mitigation and adaptation strategies. This disclosure is critical for tracking the company’s progress toward climate goals and demonstrating alignment with global sustainability initiatives.

Key aspects include:

- GHG reduction targets: The company must outline its GHG emissions reduction targets, specifying whether these are absolute (e.g., reducing emissions by a certain percentage or tonnage) or intensity-based (e.g., emissions per unit of revenue). Targets should cover Scope 1, 2, and 3 emissions.

- Scope and timeline: Targets must be defined for key milestone years, such as 2030 and 2050, in line with international climate commitments. The company should specify its baseline year and explain how future targets may evolve based on changes in market conditions, customer behavior, regulatory factors, or technological advances.

- Science-based targets: Companies must indicate whether their targets are science-based (aligned with limiting global warming to 1.5°C) and explain the methodologies and frameworks used to set these targets. This might involve referencing recognized frameworks such as the Science-Based Targets Initiative (SBTi) and sector-specific decarbonization pathways.

- Progress tracking: Disclosure should include an overview of the company’s progress towards its targets, highlighting achieved milestones, ongoing initiatives, and any challenges faced in meeting set goals.

This disclosure ensures that stakeholders can assess whether a company’s climate targets are both ambitious and credible.

E1-5 Energy Consumption and Mix

E1-5 requires companies to provide a detailed disclosure of their total energy consumption and energy mix. This metric is essential to understanding the company’s reliance on fossil fuels versus renewable energy sources, and its exposure to energy-related climate risks.

Brief summary:

- Total energy consumption: This should be provided in absolute terms (MWh) and should be broken down by source:

- Fossil sources: Includes energy derived from coal, oil, and gas. Companies with operations in high-impact sectors must provide additional disaggregation by specific fuel types (e.g., coal, petroleum products, natural gas).

- Nuclear sources: The amount of energy consumed from nuclear power.

- Renewable sources: The company must break down its renewable energy consumption, including self-generated renewable energy (e.g., solar panels on company facilities) and purchased electricity from renewable sources (e.g., wind or hydro).

- Energy intensity: For companies operating in high climate impact sectors, energy consumption should be reported as energy intensity, calculated as energy consumption per unit of net revenue. This helps stakeholders assess the company’s energy efficiency relative to its financial performance.

- Energy efficiency improvements: Companies should disclose any improvements in energy efficiency over the reporting period, which may result from energy-saving technologies, operational changes, or energy management strategies.

- Renewable energy share: The company should specify the percentage of its total energy consumption that comes from renewable sources. A higher share of renewable energy reflects better alignment with global climate goals and reduces the company’s reliance on fossil fuels.

By disclosing energy consumption and mix, companies provide critical insight into their energy transition efforts and progress toward achieving a low-carbon business model.

E1-6 Gross Scopes 1, 2, 3, and Total GHG Emissions

E1-6 is very detailed and focuses on the detailed reporting of a company’s total greenhouse gas (GHG) emissions, including Scope 1, 2, and 3 emissions. This disclosure provides an essential metric for assessing the direct and indirect climate impact of a company’s operations.

Large parts of the discloser requirements are described in the AR section of ESRS E1-6 and includes for example tables to us to report. (These tables are included automatically in Mentcon model for ESRS).

Summary of what to report:

- Scope 1 emissions: These are direct GHG emissions from sources owned or controlled by the company, such as fuel combustion in vehicles or manufacturing processes. Companies must disclose Scope 1 emissions in metric tonnes of CO2 equivalent (CO2e), giving a clear picture of their operational emissions.

- Scope 2 emissions: These are indirect emissions from purchased or acquired energy (e.g., electricity, heating, cooling). Companies must report both location-based emissions, which are based on the average emissions intensity of the grid, and market-based emissions, which take into account specific energy contracts or renewable energy certificates.

- Scope 3 emissions: These cover indirect emissions from activities along the company’s value chain, both upstream and downstream. This can include emissions from purchased goods and services, transportation, business travel, and product end-of-life. Scope 3 emissions often represent the largest portion of a company’s total carbon footprint and are critical in understanding full climate impact.

- Total GHG emissions: The company must also disclose its total emissions by summing Scopes 1, 2, and 3. This total provides a holistic view of the company’s carbon footprint and progress toward its climate targets.

In addition to these figures, companies are required to provide year-over-year comparisons and explain any significant changes in emissions due to operational changes, acquisitions, or divestitures. They must also reconcile emissions with their GHG reduction targets to ensure transparency in their climate mitigation efforts.

E1-7 GHG Removals and GHG Mitigation Projects Financed Through Carbon Credits

E1-7 requires companies to disclose their involvement in GHG removals and carbon credits to support their climate mitigation goals. This focuses on the actions a company is taking to neutralize or offset its emissions.

Key elements of the disclosure include:

- GHG removals: Companies must report the total volume of GHG removals achieved, either through direct actions within their operations or via contributions to projects within their value chain. This could involve investments in carbon sequestration projects such as reforestation, soil carbon storage, or carbon capture and storage (CCS) technologies.

- Carbon credits: Companies that finance climate change mitigation projects outside their value chain through the purchase of carbon credits must disclose the total amount of credits purchased. They must specify the quality and verification standards of the credits, ensuring they align with recognized frameworks.

- Voluntary and compliance markets: Companies must clarify whether the carbon credits were purchased through voluntary carbon markets or compliance-based schemes (such as EU Emissions Trading System). This distinction helps in understanding the nature of the carbon credits and how they align with the company’s climate goals.

This disclosure is critical for assessing the integrity of any claims of carbon neutrality or net-zero targets. Companies must explain the role of carbon credits in their climate strategies and ensure these credits do not reduce the ambition of their direct GHG emission reductions.

E1-8 Internal Carbon Pricing

E1-8 focuses on a company’s use of internal carbon pricing as a tool to manage climate-related risks and incentivize climate-friendly decision-making within the organization.

Companies must disclose (if using internal carbon pricing):

- Type of internal carbon pricing schemes: This could include the use of a shadow price, which assigns a notional cost of carbon to business activities to guide investment decisions, or an internal carbon fee, where business units pay a fee based on their carbon emissions, with funds reinvested in sustainability projects.

- Scope and application: The disclosure should explain where the carbon pricing scheme is applied, such as in CapEx decisions, R&D, operational efficiency improvements, or specific geographies and business units. It should also indicate the level of carbon pricing used and how it is determined.

- Link to targets and decision-making: Companies must describe how internal carbon pricing supports their climate policies and targets. For instance, a higher internal carbon price may accelerate decarbonization efforts by encouraging investment in low-carbon technologies or the shift to renewable energy.

- Emissions covered: Companies should disclose the scope of their emissions covered by internal carbon pricing (e.g., Scope 1, 2, or 3) and the total GHG volume associated with this mechanism. This ensures transparency in how internal carbon pricing is influencing corporate behavior and carbon reduction outcomes.

E1-9 Anticipated Financial Effects from Material Physical and Transition Risks and Potential Climate-Related Opportunities

This disclosure requirement focuses on the financial implications of climate-related risks and opportunities, particularly in the context of physical risks (e.g., extreme weather) and transition risks (e.g., regulatory changes, market shifts). Companies must provide a detailed analysis of how these risks could affect their financial performance over the short, medium, and long term.

The company must disclose (if climate change and/or mitigation is material from a financial perspective for the company):

- Anticipated financial effects from physical risks: This includes both acute risks (e.g., storms, floods, wildfires) and chronic risks (e.g., rising sea levels, changing temperature patterns). Companies must quantify the monetary value of assets at risk, disaggregated by acute and chronic risks, and describe how their operations and revenue streams could be impacted.

- Financial effects from transition risks: These include risks associated with the shift to a low-carbon economy, such as regulatory changes, technological advancements, and market shifts toward sustainable products. Companies must provide a breakdown of assets at risk and potential liabilities, particularly in sectors exposed to carbon pricing, emission regulations, or stranded assets (e.g., fossil fuel assets that may lose value).

- Opportunities: Companies must also disclose any climate-related opportunities, such as cost savings from energy efficiency, new markets for low-carbon products, or demand for adaptation solutions. These opportunities should be quantified where possible and aligned with the company’s strategic goals.

Video explaining ESRS E1 Climate change

This video from a consulting company specialized on helping companies achieve climate targets and are well aligned with ESRS E1 and Mentcon model for ESRS, (even if there they leaved out 3 the sections of disclosure requirements in this video). The interesting parts starts at 9.45 min into the video.

How does ESRS E1 Climate Change interact with other standards within ESRS?

ESRS E1 Climate Change is designed to work in conjunction with other European Sustainability Reporting Standards (ESRS) to provide a comprehensive framework for reporting on sustainability issues, including the specific challenges and implications of climate change.

Integration with Other Environmental Standards: ESRS E1 closely interacts with other environmental standards such as ESRS E2, which covers emissions like ozone-depleting substances (ODS), nitrogen oxides (NOX), and sulphur oxides (SOX). While E1 focuses on greenhouse gases and climate-related impacts, E2 addresses broader air emissions that also contribute to climate change.

Connection with Social Standards: The impacts of climate change mitigation and adaptation efforts on the workforce and communities are considered under social standards like ESRS S1, S2, S3, and S4. These standards cover how transitions to a climate-neutral economy affect various stakeholders, including workers in the company’s own workforce, those in the value chain, affected communities, and consumers and end-users.

Linkages to Water and Biodiversity Standards: ESRS E1 is also closely related to ESRS E3 (Water and Marine Resources) and ESRS E4 (Biodiversity and Ecosystems). E1 addresses the acute and chronic physical risks arising from water and ocean-related hazards as part of climate change adaptation strategies. Meanwhile, E4 focuses on the impacts of climate change on biodiversity and ecosystems, illustrating the interconnectedness of climate actions and ecological health.

Alignment with General Disclosure Requirements: As per ESRS 2 General disclosures, the disclosures under ESRS E1 should be presented alongside or integrated with general sustainability disclosures. This includes governance, strategy, and impact, risk, and opportunity management, ensuring that climate change considerations are woven into the broader strategic and operational framework of the undertaking.

Complementary Disclosure: The specific disclosures related to climate change under ESRS E1 are designed to complement the disclosures under ESRS 2, particularly concerning material impacts, financial risks and opportunities and their interaction with the company’s strategy and business model. Companies may opt to present these disclosures alongside other relevant disclosures within the same topical standard to provide a cohesive understanding of how climate-related factors are integrated into their overall sustainability strategy.